This Is Why The Future of Insurance Distribution Is Embedded

Embedded insurance is emerging as a new, seamless way to distribute insurance services and to deliver greater value to the market for the benefit of all its stakeholders. For insurers, it holds a trillion-dollar opportunity with the potential to create new revenue streams and lower distribution costs, by focusing more on the mid-market. For end customers – individuals, families, and firms – it is about getting more affordable and relevant insurance at the right time and place.

Thanks to the more modern, flexible ways of insurance distribution that almost feel like part of people’s everyday life, the time has passed over the age-old maxim which believed that “insurance is sold, not bought”. We arrived at a new era where insurers can target buyer segments they have never been in before.

What is embedded insurance?

To put it simply, the embedded insurance concept bundles coverage or protections within the purchase of a product or a service itself, offered in real-time or at the point of sale. For example, when your car rental company offers collision damage waivers on their website, or when you buy a new mobile phone and your selected package includes protection against theft, these are all examples of natively embedded insurance or “Insurance-as-a-Service” (IaaS).

With the words of Simon Torrance,

“Embedded Insurance means abstracting insurance functionality into technology to enable any third-party product or service provider or developer in any sector to seamlessly integrate innovative insurance solutions into their customer propositions and experiences, either as complementary add-ons to their core offerings or as new native components.”

For many end customers, the idea of purchasing a one-off insurance policy to protect a new possession can feel like a burdensome, unnecessary effort. By contrast, insurance products that are natively embedded in other, non-insurance product purchases allow customers to protect themselves against uninsured losses with unprecedented low (or even no) involvement, giving them increased peace of mind.

This contrast contributes to a so-called protection gap between the amount of insurance that could have been purchased and the insurance that is actually bought, especially in the risk pools of natural catastrophe, mortality, and health care. According to the Swiss Re Institute’s research, this protection gap is worth $1.2 trillion, and it has more than doubled since 2000.

Insurance companies should proactively identify these protection gaps and seek to embed their products into broader ecosystems, where they can engage with digital-savvy and relevant consumers at their preferred time and place, making this a win-win situation for both the consumer and the insurer.

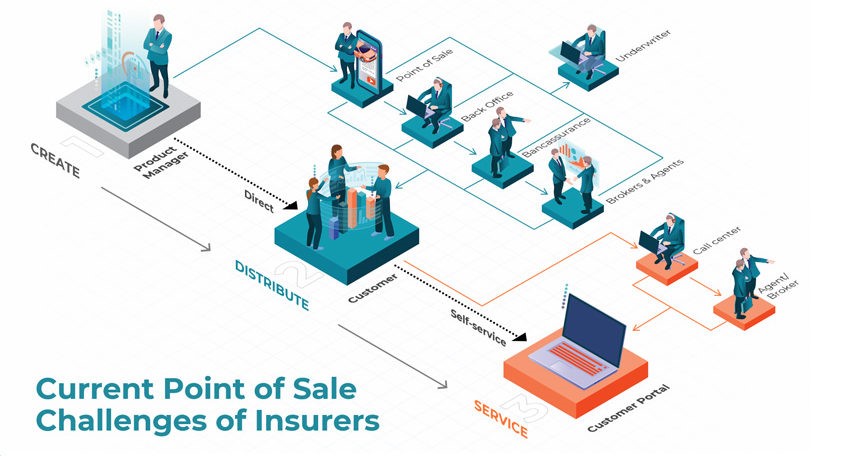

Innoveo – Current Point of Sale Challenges of Insurers

Benefits for all stakeholders

Today, insurance companies have the ability to embed their products virtually anywhere there is a risk situation through open APIs that enable other software businesses to plug in. By integrating their products into platforms with large customer bases, insurers cannot only deliver personalized policies at the most convenient time for the customer, but they also gain access to fresh customer data to perform real-time risk assessments and calculate more accurate pricing.

As André Cohen, Innoveo‘s Solution Development Director explains,

“During one of our most recent embedded insurance projects at Innoveo, we delivered an insurance marketplace with an end-to-end policy admin system and an API architecture that enables our Tier 1 customer to easily plug into partner ecosystems and have their products distributed across 24 states in the USA. In a different, European project, we helped our Tier 1 customer to white-label and distribute their auto insurance product on car manufacturer affinity partner websites such as Tesla, Audi, or Volkswagen at the point of sale.”

Overall, the embedded insurance concept provides a competitive advantage and enables insurers to thrive in today’s B2B2C environment, while also lowering acquisition costs. The insurers that will win this advantage should be prepared to develop a deep understanding of both the manufacturer, the supply chain, and its customers. But whether insurers are innovating with in-house teams or working with insurtech startups like Innoveo, embedded insurance provides a myriad of ways insurers can work collaboratively to differentiate and expand their offerings into emerging digital ecosystems.