FINANCIAL PROJECTIONS CONSULTING

Startup

The ultimate guide to financial modeling for startups

Do you have a startup and do you want to build a sustainable financial future? Discover the best practices in the ultimate guide to financial modeling for startups.

We have three very easy questions for you:

- Do you want to build a (financially) sustainable business?

- Are you looking for funding?

- Do you want to avoid going bankrupt?

Probably you have answered yes at least once. If you have founded your own company, probably yes applies to all three questions.

To cover all three having (some form of) a financial model is crucial. Whatever the reason is for you ending up at looking at this article, apparently also for you financial modeling is an important topic, otherwise you wouldn’t be here, right? 😉

Well, you have come to the right place! Having supported around a thousand startups and scale-ups with their financial models over the past couple of years with the EY Finance Navigator team, we have written everything you need to know and all the best practices available around financial modeling for starting businesses: the ultimate guide to financial modeling for startups!

NOTE: in this article we are not sharing any financial modeling templates. Why? There are tons and tons of them already available online: simply look for ‘financial model template’ on the web and you are done.

This article is written with the purpose of doing something a template cannot do for you: helping you understand the different elements and technicalities of a startup’s financial model, learn how to fill it in and do checks on your data so you are able of making sense out of the outcomes yourself. And if you need additional support, feel free to reach out using the contact form.

Three reasons for having a financial model as a startup

Why it’s important to build an economically viable business

Before we dive into the technicalities and different elements of a startup’s financial model we are going to broaden our view a bit and address why forecasting in general is an important topic for startups. Almost all companies perform some kind of financial planning or budgeting, but there are particular reasons why a financial plan is important for startups specifically:

- You need one to build an economically viable business. Why? Because by quantifying (and then validating) your business plan and business model, assumptions and vision you are able of finding out whether you can turn your ideas into a sustainably operating business.

Moreover, if you build different versions (“scenarios”) you are better prepared for the future, especially if things do not go the way you planned. What if you launch half a year later? Answering such a question in your “worst case scenario” helps you anticipate how your cash flow, profitability and funding need are impacted. - You need one as part of the fundraising process. Financiers will typically ask you for a financial plan when you engage with them to raise funding, whether them being angel investor, VC, bank or subsidy provider. Certain investors will require more details then other, but building a model is wise even if you only need to provide them with high-level data.

Why? Because it helps you answer the tricky questions a financier might have when he or she dives into your business case. Moreover, how are you planning to raise funding if you did not properly calculate how much funding you actually need? - You need one to inform yourself and shareholders. How do you know how your company is doing if you don’t have any targets to achieve or steering information to compare against? How are you going to update your shareholders on how you are spending their money and whether you are performing as promised without any financial plan to benchmark against? You will need a forecast to do so.

Do these reasons apply to your case as well? Good! Then definitely continue reading…

Two different approaches to financial modelling for startups

Building a financial model is not difficult, but how to get the numbers?

Often building a financial model is not really an issue. The amount of templates you can find online are countless and there’s always someone Excel-savvy around to help you out with the technicalities. The REAL problem (and question we get most often) is: how to get to the numbers?

…how do you forecast sales?

…what is the market size of my sector?

…how much should I spend on marketing?

Etc.

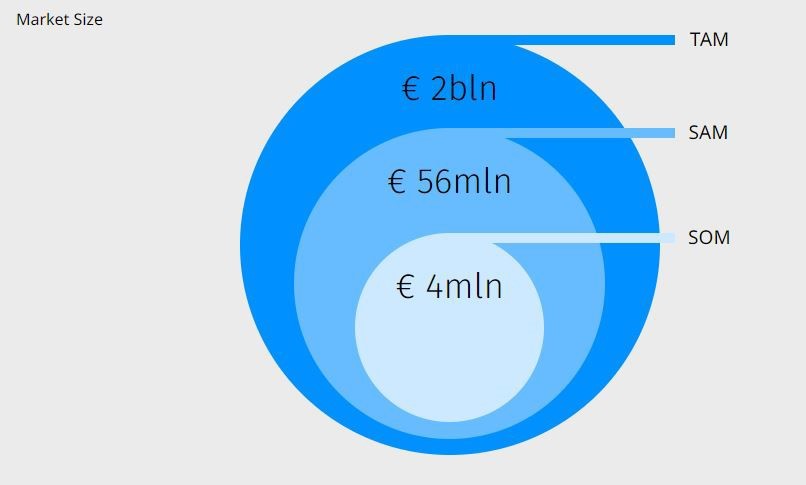

There are two main methods to answer these questions: top down forecasting and bottom up forecasting.

Top down forecasting

Often building a financial model is not really an issue. The amount of templates you can find online are countless and there’s always someone Excel-savvy around to help you out with the technicalities. The REAL problem (and question we get most often) is: how to get to the numbers?

…how do you forecast sales?

…what is the market size of my sector?

…how much should I spend on marketing?

Etc.

There are two main methods to answer these questions: top down forecasting and bottom up forecasting.

Based on the sales targets you define using the TAM SAM SOM model the next step is to estimate all costs that are needed to build or deliver your product or service and all expenses that are needed to perform all sales and marketing, research and development, and general and administrative tasks for your company to stay alive.

When estimating these you obviously aim for profitability within a reasonable timeframe. In other words: at some point all costs and expenses should not exceed your revenue targets anymore so that you get to a positive EBITDA (earnings before interest, taxes, depreciation and amortization).

Bottom up forecasting

The pitfall of the top down approach is that it might seduce you to forecast too optimistically (especially sales). Often entrepreneurs calculate SOM (equal to sales) by taking a random percentage of the market, without really assessing whether this target is realistically achievable.

A tiny percentage of a market might seem insignificant, but could be way too optimistic for instance in the year of your launch. Therefore, it could be useful to complement the top down method with the bottom up approach.

The bottom up approach is less dependent on external factors (the market), but leverages internal company specific data such as sales data or your company’s internal capacity. Contrary to the top down method, the bottom up approach begins with a micro/inside-out view and builds towards a macro view. This means a projection is made based on the main value drivers of your business.

Short example: let’s assume one of the main drivers of an online SaaS business is online marketing. One of its online marketing tactics is to advertise its product via LinkedIn. The company could define the costs per click using LinkedIn’s advertising tool, estimate the number of website visitors it will attract as a result, the conversion from website visitor to a lead, and the conversion from lead to customer.

Based on these metrics the company will have a good idea of potential sales, of course constrained by the budget available for online advertising. Performing a bottom up analysis therefore does not only force you to think about what are realistic targets for your company, but also to think about the ways in which you will spend your resources.

With the bottom up approach, you estimate revenues, costs, expenses and investments in the same way as described above: based on the resources at hand and the company data that is available. The pitfall of the bottom up method though is that it might fail to show the optimism needed to convince others of the potential of your company.

If you are a startup founder and you are looking to raise funding, the bottom up approach might not do the trick. Investors usually expect startups to grow fast and gain significant market share rapidly. The bottom up method might fail to reflect that.

It is difficult to create a forecast with a steep growth curve if every sale has to be rationalized and if its point of departure is the maximal capacity of your company (or budget for advertising purposes). With the bottom up approach it is hard to take into account factors such as virality or word of mouth. Moreover, the whole reason why external financing is needed, is often to expand capacity and grow faster than a company would do organically.

Therefore, when you build your startup’s forecast it could be advisable to combine both the bottom up and top down methods, especially when you plan to achieve a strong growth curve by means of external funding. Use the bottom up method for your short term forecast (1-2 years ahead) and the top down method for the longer term (3-5 years ahead). This makes you able to substantiate and defend your short term targets very well and your long term targets demonstrate the desired market share and the ambition an investor is looking for.

Assumptions

No matter what approach you use to build your startup’s financial model, it is crucial you are able of substantiating your numbers with assumptions. As a startup, historic data is often not available so you need to be able to present the ‘proof’ behind your numbers.

This will also help you when you start discussing with investors, as they are typically interested in knowing the reasoning behind your numbers. They are considering to put money in your company, so you do not want to give them the feeling you are selling baloney!

Assumptions can be anything that validate your numbers: market research, web search volume, contracts with suppliers, pricing validation, historic sales, conversion rates, bills of materials, website traffic, etc. It could be useful to create a “data room” (e.g. a Drive folder) in which you collect these kinds of evidence. By doing so, you are slowly building a library that underpins all the numbers you have put in your model and you are well prepared in case an investor might request a due diligence process.

Now, that is more than enough background to get started. Let’s get to it: the financial overviews a good financial model (of a startup) should include!

Three outcomes of a startup’s financial model

Every sector, company, business owner and investor is different, but a good financial model usually contains at least the three outputs.

Every sector, company, business owner and investor is different. All of them have their own interests and all of them value different metrics. From that perspective it is thus fair to say every financial model has its own characteristics. Therefore it is possible to customize every model to its user.

However, a good financial model usually contains at least the three following outputs: the financial statements, an operational cash flow forecast and a KPI overview.

Financial statements

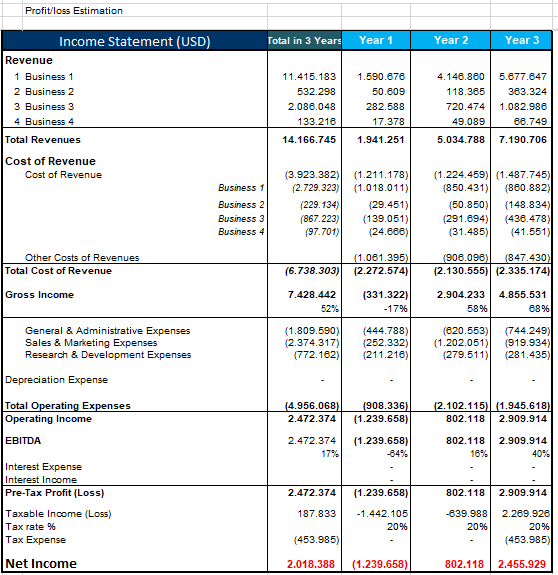

Any decent financial model includes a forecast of the three financial statements: the profit and loss statement (P&L), the balance sheet (BS) and the cash flow statement (CF). The financial statements are the generally accepted way of communicating financial information across companies, banks, investors, governments and basically anyone that needs to show and/or understand financial performance in some way. Since any financial professional is able of interpreting financial statements having a forecast of them in place is typically a requirement in practically any fundraising process.

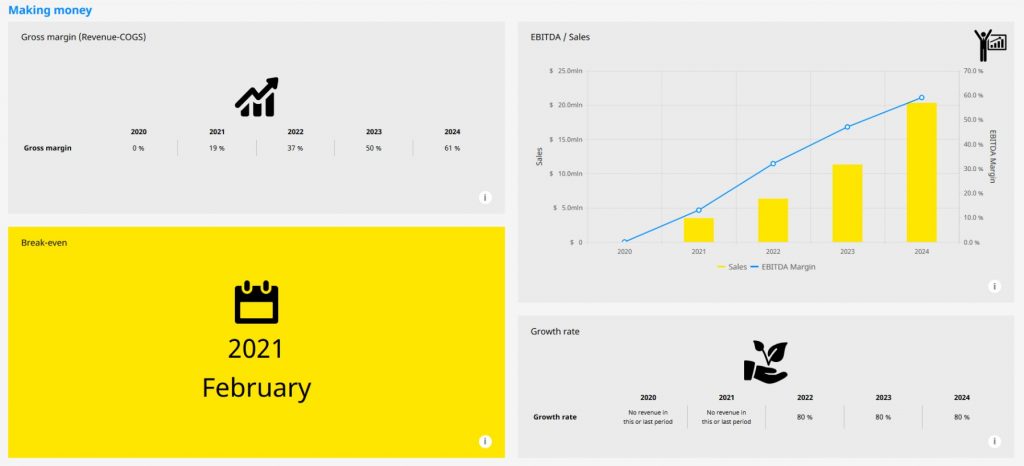

The profit and loss (or income) statement is basically an overview of all the income and costs your company has generated over a specific period of time and shows you whether you are profitable or not.

The P&L shows several crucial performance metrics such as the gross margin, EBITDA and net margin. EBITDA (earnings before interest, taxes, depreciation and amortization) is very important for investors as it provides insights in the operational performance of a company and allows them to compare efficiency when comparing different companies. The P&L can be used for comparing different time periods, budget vs. actual performance, performance against other companies etc. and can therefore show weak or strong performance.

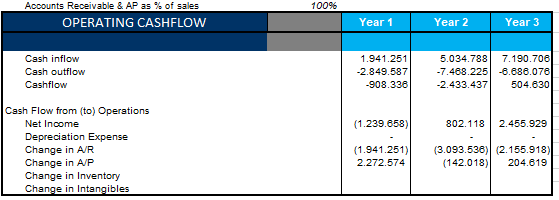

The cash flow statement shows all cash going in and out of a company over a specific time period. The cash flow statement consists of three different parts: the operational cash flow, the investment cash flow and the financial cash flow. The separation between these three categories provides you with insights on where money is going in and out of the company.

Operational cash flow shows the cash inflows and outflows caused by core business operations. Investment cash flow shows changes in investments in assets and equipment. In most cases (concerning startups) investment cash flow will have a cash outflow (because investing in assets costs money), but in some cases investment cash flow can also be positive in case a company is divesting (selling assets, e.g. selling real estate).

Financial cash flow relates to cash changes arising from financing activities. Cash inflow occurs in case of raising capital (such as loans or equity) and cash outflow occurs in case dividends are paid or when interests on cash financing are paid (e.g. to bondholders).

The cash flow statement allows management to make informed decisions on business operations and allows it to prevent and monitor company debt. Moreover it helps define a company’s investment needs and supports the timely payment of expenses and debts.

Operational cash flow overview

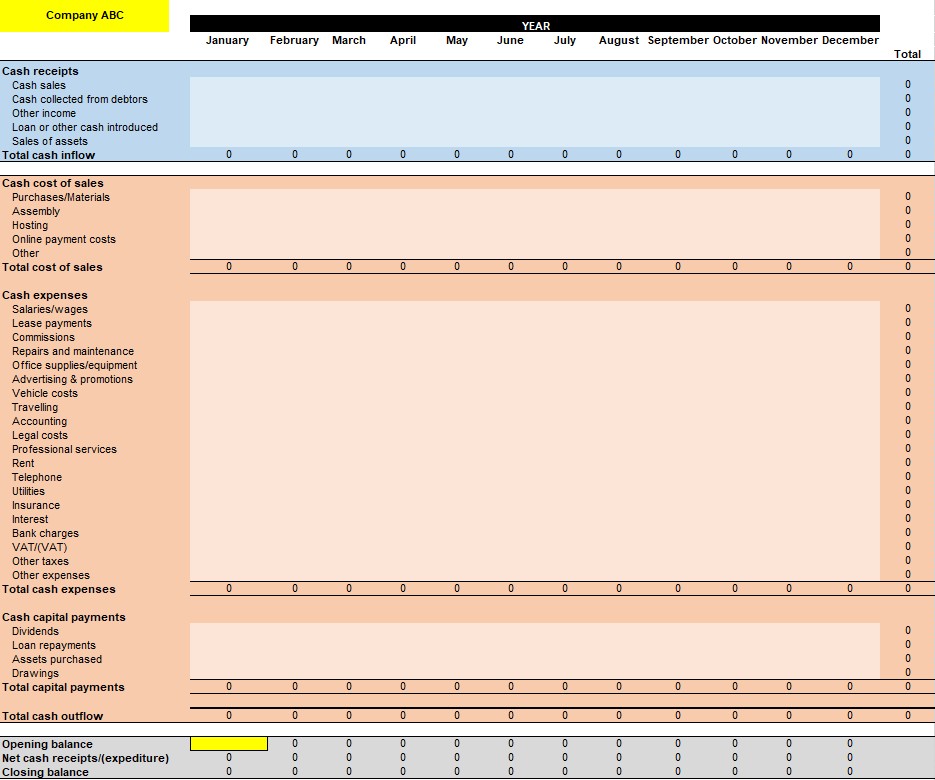

For fundraising purposes a forecast of the financial statements is typically shown on a yearly basis. Monthly overviews are in most cases not really needed, because for early-stage startups it is more about showing the long term growth potential than about giving an insight in monthly operations.

However, for the actual day to day financial management of your company it is useful to include an operational cash flow for the coming 12 months ahead in your financial model.

Why? Because it addresses questions yearly financial statements cannot answer, for instance about the timing of cash in and outflows. This is important to anticipate (see section ‘Working Capital’ below).

Moreover, it provides you with an opportunity to track your actual performance versus your expected budget on a monthly basis, which helps you cut costs (if needed) and anticipate to potential cash dips months ahead.

To build an operational cash flow forecast you simply list all the categories of cash inflows and outflows (for instance in an Excel), add a starting balance (the cash you own at this very moment) and see what remains at the end of each month.

An example can be found below. If you would also add columns where you can enter your actual numbers (against the forecasted cash in-and outflows) you are able of tracking performance over time and anticipate cash issues early on.

KPI overview

The outputs of a startup’s financial model typically also include some company and/or sector specific KPIs (key performance indicators). As the name already implies KPIs are crucial metrics for your business.

KPIs do not only matter for an investor, but also for you as a company owner. Based on these metrics you track the performance of your company, experiment with different acquisition channels, business models and cost structures, and you use them to make you and your co-founders laser-focused on the targets you defined.

There are KPIs that show sales and profitability performance (such as revenue growth rate, gross margin, EBITDA margin or profits), KPIs related to cash flow and raising investment (such as the burn rate, runway and funding need breakdown) and company or industry specific KPIs.

SaaS companies for instance typically estimate and track, amongst others, the customer life time value (LTV), customer acquisition costs (CAC), LTV/CAC ratio and the churn rate. For SaaS businesses, these are crucial.

For your business or industry some other metrics might be more important. Perform a bit of research on the web, think about the most important drivers of your company and identify the ones most relevant to you and to potential investors. Include these in your financial model as well.

The inputs to a startup’s financial model

What are the six common elements that typically serve as the input sheets of a financial model?

The outputs discussed above do not all of a sudden appear out of nothing, obviously. They are the result of many calculations taking place in the background of a financial model, based on the data entered into different input pagessubstantiated by the assumptions and research performed by the person filling in the financial model.

In this article we are not discussing all the calculations that take place in a financial model, as that would be a heck of a job! As mentioned earlier, we focus on helping you understand the different elements and technicalities of a startup’s financial model, learn how to fill it in and make sense out of the outcomes.

If you want insights in the calculations you can download a financial modeling template online. If you do not want to worry about (errors in) calculations at all, try out our financial planning software for startups.

Below we have listed six common elements that typically serve as the input sheets of a financial model. One element we have left out as an input sheet is what you could call the financial model’s ‘settings’.

These define the setup of the complete model and include things such as the forecasting period (which is typically 3-5 years, sometimes ten for certain industries), the currency used, taxes that might apply, etc.

Before moving to the different inputs of a startup’s financial model, it is important to realize financial modeling is not a goal in itself. It should be a means to an end. And that end is typically to get more insights in the financial side of building a business, whether those insights are meant for yourself or for a potential investor.

A financial model is a quantification of your overall business and should therefore be a reflection of your strategy, business model and vision. It is therefore fair to say your financial model and business model canvas are two sides of the same coin.

If you are ever in doubt on what to include in your financial model or if you need to take a step back from the numbers, you can use your business model canvas as a tool to help you think about your financial plan.

Revenues

Any decent financial model includes a forecast of the three financial statements: the profit and loss statement (P&L), the balance sheet (BS) and the cash flow statement (CF). The financial statements are the generally accepted way of communicating financial information across companies, banks, investors, governments and basically anyone that needs to show and/or understand financial performance in some way. Since any financial professional is able of interpreting financial statements having a forecast of them in place is typically a requirement in practically any fundraising process.

The profit and loss (or income) statement is basically an overview of all the income and costs your company has generated over a specific period of time and shows you whether you are profitable or not.

The P&L shows several crucial performance metrics such as the gross margin, EBITDA and net margin. EBITDA (earnings before interest, taxes, depreciation and amortization) is very important for investors as it provides insights in the operational performance of a company and allows them to compare efficiency when comparing different companies. The P&L can be used for comparing different time periods, budget vs. actual performance, performance against other companies etc. and can therefore show weak or strong performance.

The first (and maybe also most fun) input sheet of a financial plan is the revenue forecast. Revenue projections can be tricky though, for instance when you have not achieved any sales in the past yet. So how would you go about this? For a deep dive we would recommend to have a look at our earlier article on how to create a killer sales forecast for your startup, but we will present the key takeaways below.

Forecasting revenues is typically performed using a combination of the top down (TAM SAM SOM model) and bottom up methods which have been discussed earlier in this article. Use the bottom up method for your short term sales forecast (1-2 years ahead) and the top down method for the longer term (3-5 years ahead). This makes you able to substantiate your short term targets on a detailed level, while at the same time your long term targets demonstrate the desired market share and the ambition an investor is looking for.

If you find it difficult estimating demand at all one way of tackling this is to perform keyword research. Keyword tools give you insights in the search volumes for keywords that relate to your offering. They can show you per city, country, continent (whatever you want) how much monthly searches are performed for that specific keyword on the internet.

This can give you a good indication on demand for certain offerings, compared across different countries. You could try for instance the keyword tool Ubersuggest. If you sell 3D printers, you could search “buy 3D printer” and see how much people search for these words per month.

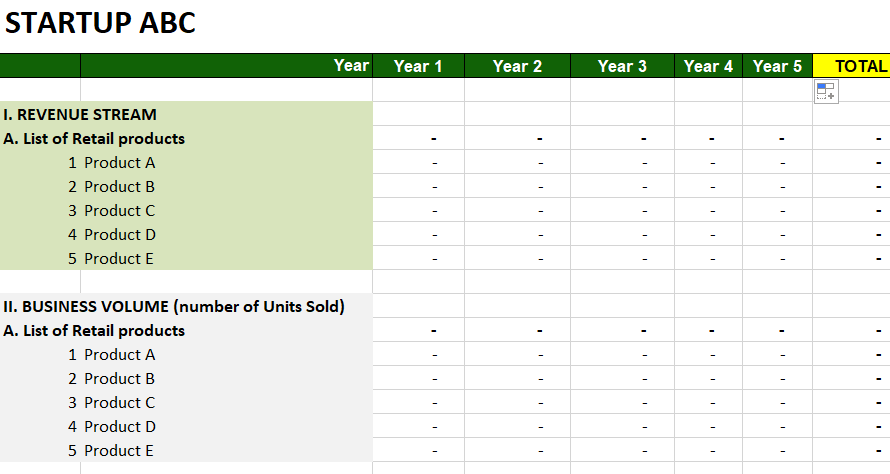

Now you know the approaches to forecasting, this is how you actually put your forecast down on paper:

- List all the products or services that you are selling.

- Determine in which units you want to present your sales: for a soda producer, this could for instance be bottles sold, but also liters sold.

- Forecast per sales unit the number of units sold. This is based on the top down and bottom up analysis you have performed above.

- Add selling prices. Check out our article on new product pricing strategies if you want to learn more on how to determine pricing.

You could for instance end up with something that looks like this if you would prepare the forecast in Excel:

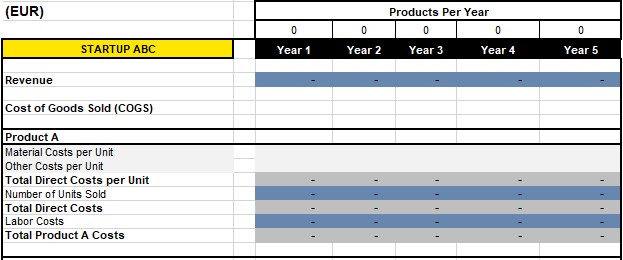

Cost of goods sold (COGS)

Cost of goods sold (COGS) are those costs that undoubtedly need to be made in order for a company to deliver a service or produce a good. Without these costs, the product or service would simply not exist.

COGS differ based on the type of offering you sell. For a company that sells tangible products they would include for instance the costs of the materials used in creating the good. For a company that sells consultancy hours they would include the personnel costs of the employees delivering the service.

For a SaaS business COGS are different compared to ‘normal’ businesses as there is no regular production or service delivery process involved. However, also SaaS companies definitely incur COGS, such as hosting costs, customer support and onboarding costs, and online payment costs. From these examples you can notice that all of these costs have to be incurred in order to produce the good or deliver the service.

Not sure how to forecast COGS? One way of tackling this, is by looking at the sales targets defined in your revenue forecast. Let’s assume you sell a tangible good. From creating the revenue projections you know already how many units of sales you aim to have. You then add per unit of sales the costs of raw materials and labor costs involved in producing those goods.

Example: if you sell plastic bottles, you could calculate how much plastic (in grams) you need per bottle and what would be the price of a kilogram of plastic. Moreover, you need to know how much paper label you need per bottle and what is the price of that. Also, you need to know the costs of the cap.

If you know all of these costs required to produce one bottle you can multiply them by the total number of bottles sold. Finally you add the personnel costs for employees that are involved in production.

If you would prepare this in Excel it would probably look something like this:

How to forecast COGS also depends on your business model. Sometimes it would make more sense to forecast COGS on total level, for instance per month. Or they could be a percentage of your revenues (for instance when you work with sales commissions). Our financial planning software for startups includes different types of COGS forecasting.

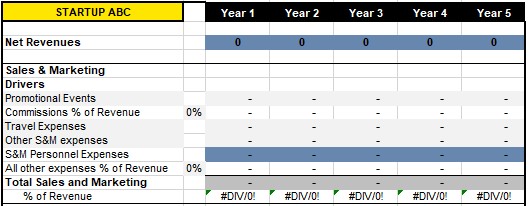

Operating expenses (OPEX)

Operating expenses are those expenses that a business incurs as a result of performing its normal business operations. Unlike the cost of goods sold, they are not necessarily needed to produce the goods that are sold or to deliver the services promised. They include costs related to the supporting and operational side of business, such as sales and marketing, research and development and general and administrative tasks.

Typical operating expenses for startups include: events, travelling, legal costs, online marketing, payroll costs (of employees not part of COGS), accounting, rent, utilities, insurance, prototyping, patent costs, IT costs, office supplies, promotional materials, etc.

If you are not sure about which expenses you might incur in the long term, you could always save a certain percentage of your revenues for the different expense categories. E.g. you could include 10% of your yearly revenues on a budget for sales and marketing activities.

Most important is that your spending on operating expenses aligns with your company strategy. Is the growth of your company heavily reliant on online marketing? Then you would expect significant spending in that category.

An example of what an operating expenses forecast could look like for instance for spending on sales and marketing, can be found below.

Personnel

Personnel is probably one of the easier forecasts to build. With your personnel forecast you project the number of employees hired including their respective salaries, additional benefits and payroll taxes. To make personnel forecasting more simple you could split up your personnel into different categories, for instance:

- Direct labor: here you include the employees that will be solely engaged with the production of the goods sold or services delivered. Think of engineers and technicians for companies selling tangible hardware products, a junior advisor in a consultancy company, or customer onboarding personnel in a SaaS business. These costs are not part of operating expenses but are part of the cost of goods sold.

- Sales and marketing: for instance sales managers, marketing managers, copywriters, social media experts, etc. These employees are part of your operating expenses.

- Research and development: R&D managers, (software) engineers, technicians, etc. These employees are part of your operating expenses.

- General and administration: here you include back office and C-level personnel, such as the CEO, CFO, CMO, secretaries, bookkeepers, etc. These employees are part of your operating expenses.

An example of what a personnel forecast could look like, for instance for personnel working on sales and marketing, can be found below.

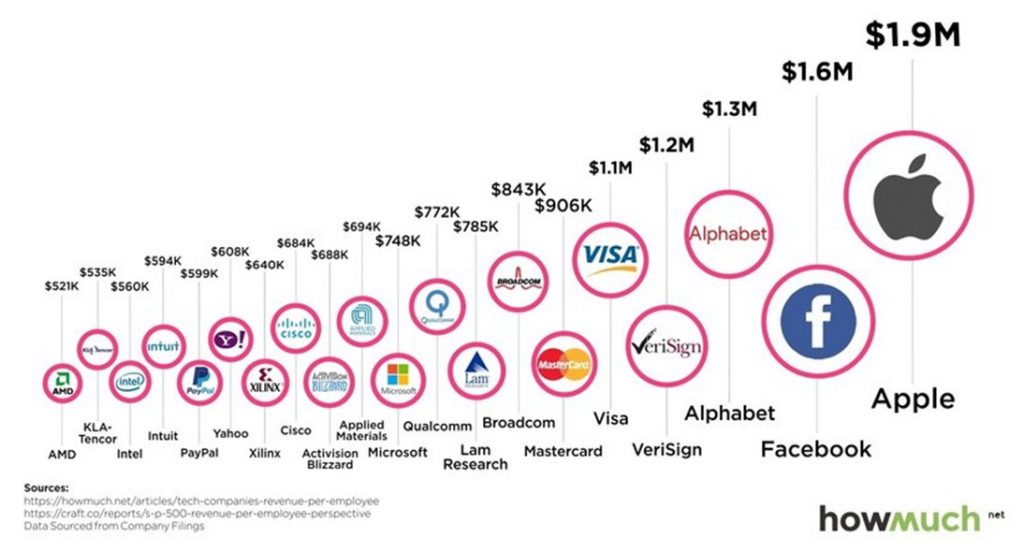

If you want to check whether your personnel forecast is realistic, you could divide your projected revenues in a given year by the number of employees (‘FTEs’ or full time equivalents) for that year. This tells you how much revenue you expect to generate per employee and provides a solid basis for comparison with competitors and industry leaders.

When your revenue per employee is at a similar level compared to the top twenty tech companies (see the graph below) already in just a few years after your launch, this is a strong indicator that you might be too optimistic regarding your expected revenues or that you might invest insufficiently in personnel.

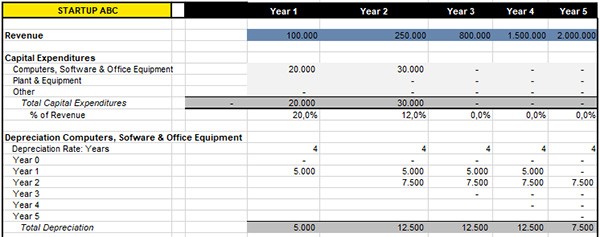

Investments in assets (capital expenditures)

The fifth input sheet to your startup’s financial model are the investments in assets (or: capital expenditures). Capital expenditures are funds used by a company to acquire or upgrade physical assets such as physical property, intellectual property, buildings or equipment. This type of expense is made by companies to maintain or increase the scope of their operations. They can include everything from repairing a roof to building a brand new factory.

Typical capital expenditures depend on the type of business and industry. For startups it is quite common to invest in computers, software, office equipment and machinery, but buying a building would also apply as a capital expenditure.

Many startups are incentivized to categorize their expenses as capital expenditures instead of as operating expenses. This has to do with the fact that due to an accounting technicality payments related to investments in assets are spread out over several years in the profit and loss statement (see section ‘Deprecation’ below) and therefore do not show up all at once in the year of purchase. This means they have a less visible reducing impact on profits. Be aware that the rules for categorizing expenses as assets are quite strict though!

Financing

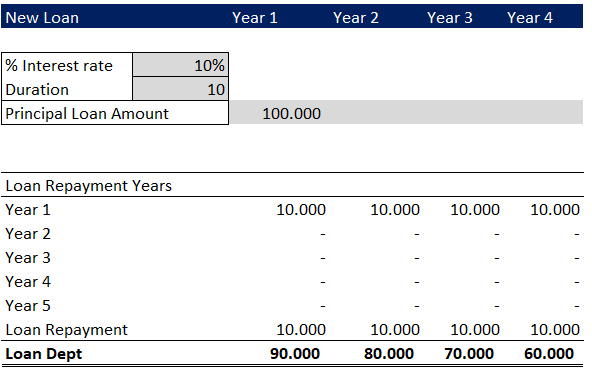

The final potential input sheet of a startup’s financial model could be a financing module. In this sheet you would add financing streams such as equity, loans or subsidies. The main goal of this would be to check the impact on your funding need when you add different types of funding in different years of the model.

When a model includes the possibility to input loans, it needs to account for the loan repayment and interest payments, as these have an impact on cash flows. Below you can find a simple example of a €100,000 loan with a duration of 10 years and an interest rate of 10%.

The six different input sheets that are discussed above are all in some way linked to the outputs of the financial model. For the financial statements specifically the links are as follows:

- Revenues impact the top line of the profit and loss statement. In the P&L you deduct all costs, expenses and depreciation from the revenues to arrive at EBIT (earnings before interest and taxes). EBIT serves as input for the operational cash flow in the cash flow statement. If you deduct interest and taxes (see section ‘Taxes’ below) from EBIT, you arrive at the net profit. Revenues even impact the balance sheet as they define the accounts receivable position.

- Cost of goods sold also turns up in the profit and loss statement. Deducting them from the revenues results in the gross margin. The gross margin can also be presented as a percentage: the higher this percentage is, the more revenue is left for covering costs that are not directly related to production. Cost of goods sold also impacts the balance sheet as they define accounts payable and inventory.

- Operating expenses show up in the profit and loss statement as well. Deducting operating expenses and cost of goods sold from the revenues results in EBITDA (earnings before interest, taxes, depreciation and amortization).

- Personnel either shows up in the profit and loss statement as a separate line or it is included in the cost of goods sold or operating expenses. Personnel involved in delivering services or producing goods end up in cost of goods sold. All other personnel is part of operating expenses.

- Investments in assets (capital expenditures) do not show up in the profit and loss statement because, accounting-wise, they are not seen as costs or expenses. They are investments and can be capitalized, meaning a company can leverage their value for several years. Therefore, they show up as something a company owns in the assets side of the balance sheet. Their value is depreciated (reduced in value) over their lifetime which is shown as depreciation in the profit and loss statement.

Even though investments do not show up as a cost or expense, investing in something does mean there is a cash outflow for your company (you have to pay, right?). Therefore investments also show up in the cash flow statement as investment cash flow. - Financing impacts the financial statements in two ways. Firstly, new financing and changes in debt shows up in the cash flow statement as financing cash flow. Secondly, interest paid on debts end up in the profit and loss statement.

The financial statements themselves are also interrelated (see image below). For that reason it could be wise to have an experienced person supporting you building your model if you do not have this experience yourself, especially if you are looking for a more complex model including supporting schemes such as the ones mentioned in the next section.

Other supporting elements of a startup’s financial model

What other elements are essential for your financial model?

As you might have noticed already, some of the elements mentioned above include some tweaking of the numbers before you get to the right information that is presented in the financial statements. Supporting schemes such as working capital, depreciation and taxes might be needed.

Moreover, when you build a financial model you automatically structure a whole lot of data which you can also use for other purposes, such as a company valuation. Therefore, below we present four elements that support a startup’s financial model.

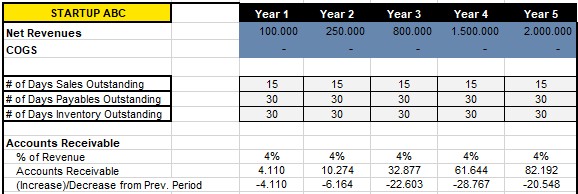

Working capital

Working capital is the capital that you need in order to sustain your daily operations. Technically speaking working capital is a comparison of the value of your current assets compared to your current liabilities.

In other words: the value of the things your company owns and that can be converted to cash on the short term (in less than one year) compared to the value of the things your company owes to others that are due on the short term (less than one year as well). Current assets include cash, accounts receivable and inventory. Current liabilities for instance include accounts payable.

Working capital is extremely important for startups, because it is a measure of both a company’s efficiency and its short-term financial health. Working capital can significantly affect cash flow, so if a company’s current assets do not exceed its current liabilities, then it may run into trouble paying back creditors in the short term. The worst-case scenario is bankruptcy.

Working capital can be impacted by payment terms. In order to assess your working capital position you should therefore not only steer your company based on revenue targets, but also on your cash flows. Forecasting for cash flow provides you with an overview of the timing of incoming and outgoing cash flows. How to do this is discussed in section ‘Operational cash flow overview’.

Why is this important? Well, when you focus only on costs and revenues and not on the timing of receiving and sending payments you could end up in serious trouble.

Consider that a large firm orders one hundred 3D printers at a startup producing a new type of 3D printers. The client expects the printers to be delivered within one month. As large firms often use long payment terms it might take up to 90 days before the startup receives the actual payment for the order.

This means that our 3D printer startup needs to finance the raw materials and production process itself. After all, the company has to deliver within 30 days, but still has to wait for 90 days before the payment is received.

If the funds required for production are not available for the startup then the order might be cancelled leaving both parties unsatisfied. If this happens consistently, the startup could go bankrupt even though orders are coming in.

Working capital is calculated based on the number of days your sales and payables are outstanding and the number of days you hold inventory before selling it. It shows up in the balance sheet. Therefore, a financial model might need a separate scheme that calculates working capital based on revenues, cost of goods sold and days outstanding.

See for instance the example of the calculation of accounts receivable below. With revenues being €100,000 in year one and payment terms of 15 days for outgoing invoices the accounts receivable position at the end of the year is €4,110.

Depreciation

Deprecation indicates the value reduction of assets a company owns. Based on the value of an asset and its useful lifetime depreciation is calculated. Depreciation is part of the profit and loss statement and impacts the value of assets on your balance sheet.

As an example, let’s say you want to buy some computers for your company. They cost you €20,000 and you can use them for four years. This means you will write off the total investment of €20,000 over a period of four years, which means you will depreciate their value with €5,000 every year for the coming four years (if they do not have any residual value left after that).

A financial model needs a separate scheme that calculates depreciation based on investments and their related useful lifetime. Below you can find an example calculation of depreciation.

As you can see, in year one €20,000 was invested in computers, software and equipment and in year two €30,000. Both are depreciated over four years, resulting in the total depreciation per year; being €5,000 for year one, €12,500 for year 2-4 and €7.500 for year five.

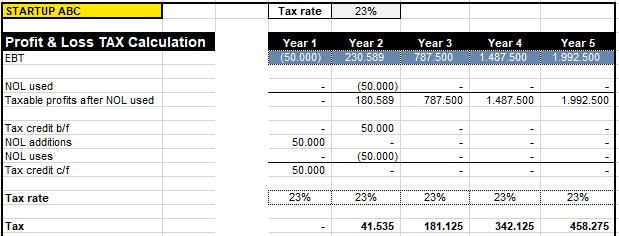

Taxes

Every company that is incorporated and registered at the Chamber of Commerce has to pay yearly taxes over its financial results: the corporate income tax. Taxes are deducted from your results in the profit and loss statement. Here you can find a list of corporate income tax rates per country.

If you want to include tax carryforwards in your financial model, you likely need a separate tax scheme as part of your model. A tax carryforward works as follows. As an entrepreneur it is likely that you have negative results in the first couple of years of operations. If you have negative results this basically means you have expenses that exceed revenues (more costs than income) leading to an operating loss. If you have a loss, there is obviously no income to be taxed by the tax authorities. This loss can be leveraged in future tax reporting periods to offset taxable income (you can ‘carry it forward’), which reduce the amount of tax you will pay in that specific tax reporting period.

Below you can find an example of a tax carryforward calculation based on a corporate income tax rate of 23%. As you will notice, year one had a negative result of -€50,000 which is settled with the positive result of €230,589 for year two resulting in a taxable profit of €180,589, resulting in a lower tax burden for that year.

Valuation

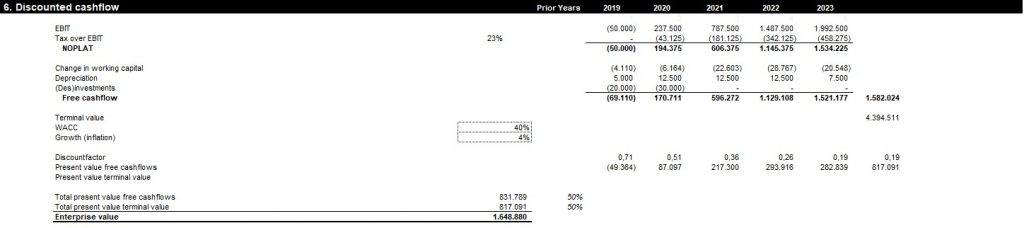

Many startups build a financial model for the purpose of raising funding. Part of the fundraising process are negotiations with an investor about the valuation of the company to be invested in. The good news is that when you have built a financial model for your company, all the ingredients are there to perform a valuation on your company as well by means of the discounted cash flow (DCF) method.

The main advantage of the discounted cash flow method is that it values a firm on the basis of future performance. This is perfect for a startup that might not have realized any historical performance yet, but expects large future earnings. During the (pre-)seed stage it is not uncommon for startups to not generate any revenues at all yet, while discussions with investors regarding ownership percentages and the accompanying valuation already take place. The discounted cash flow method is very suitable in that case, as it weighs future performance more than current performance.

The main downside of the DCF method when valuing startups is that the DCF is nothing more than a formula, a mathematical operation. This means that the quality of the valuation is extremely sensitive to the input variables of the formulas used to calculate the valuation. Moreover, it largely depends on your ability to create an accurate forecast of your firm’s future performance. After all, the future earnings are the foundation of the valuation.

A deep dive into discounted cash flow valuation is out of scope for this article. The main steps of performing a discounted cash flow valuation are presented below, but we have also written a deep dive into startup valuation:

- Step 1: create financial projections for your firm (tick in the box!).

- Step 2: determine the projected free cash flows.

- Step 3: determine the discount factor.

- Step 4: calculate the net present value of your free cash flows and terminal value by using the discount factor.

- Step 5: sum up all results of step 4.

Below you can find an example of a discounted cash flow valuation.

Depending on the desired outcomes and the corresponding complexity of your financial model you can decide whether or not to add additional schemes such as working capital, depreciation and tax carryforwards. You can look for a financial model template including these elements on the web. If you do not want to worry about these elements at all, our financial planning software for startups does all the calculations for you.

Scenarios and sanity checks

What other elements are essential for your financial model?

We have taken a look at all the different elements of a startup’s financial model. That means we are done! Right…? Not quite yet! For the pros there are some additional steps to take.

Firstly, it could be worth it to spend some time creating different versions (called scenarios) of your financial model. Entrepreneurs tend to be optimistic people, which is a good characteristic to have to keep up the energy and push through where others might quit.

Unfortunately, in many cases, the life of an entrepreneur tends to be a bit more disappointing in practice than it is on paper (at least from a financial perspective, don’t get too depressed now). Therefore, next to your default financial plan (called your ‘base case scenario’) you might want to prepare a scenario which is a bit less optimistic (your ‘worst case scenario’).

What if you launch six months later? What if sales do not ramp up as expected? What if your costs turn out to be double of what you expected? Answering such questions helps you anticipate how your cash flow, profitability and funding need are impacted in a less optimistic scenario.

Do not forget to create a ‘best case’ scenario as well. Why? You can give potential investors a sneak preview of the upside potential of your company and most importantly: it is fun to see the financial impact of aiming for the moon!

Secondly, it might be wise to perform some sanity check on your financial model to make sure you avoid common pitfalls in the financial models of startups. You can find ten common errors below:

- A mismatch between the financial model and the business plan: a financial model should resonate with the overall business strategy

- Overoptimistic or very pessimistic revenue projections: check out section ‘Revenues’ on how to forecast sales

- A funding need that is not adequately explained: make sure you include a breakdown of costs

- Underlying assumptions that are not clearly defined: you should be able to provide clarification or proof to the numbers

- Not enough employees as part of the personnel forecast: do not underestimate the number (and costs) of employees you need to build a fast-growing company

- Revenue projections which are not aligned with the market size: by definition revenues cannot be larger than the size of the market

- Operational expenses that are being left out: make sure expenses are aligned to your strategy

- Operational expenses which are misaligned with the forecasted revenues: make sure expenses resonate with revenues

- No realistic view of the gross, EBITDA and net margins: when speaking with investors, always be prepared to answer questions on your current and expected margins

- Disregarding the importance of working capital: do not underestimate the effect of payment terms on your funding need

Financing

How to raise money for your startup?

Many startups create a financial model because they are looking to raise external funding. Whether you are applying for a loan at a bank, trying to convince an investor of the potential of your firm or are applying for a subsidy or grant; in most if not all cases you will need to provide your counterparty with a financial plan.

There are different ways of raising money for your startup and these can be categorized into two main categories.

Financing via debt: an example of financing via debt can be a loan which you receive from a bank, a business or an individual where you agree on specific terms regarding payback and interest. For startups it can be difficult to receive a loan from a bank as they often do not meet the minimum criteria in terms of revenue generation and offering collateral.

Some advantages of using debt are as follows:

- The control of your company remains with you and your current shareholders.

- Interest on debt can be deducted from your tax.

- Debt often has a disciplining effect on a management team, as the resulting cash flows are limited so the management will be encouraged to be more efficient and create value.

Financing via equity: an example of financing via equity is funding you would raise from an angel investor or a VC in return for shares of your startup. For startups, financing via equity is more common than debt financing, because receiving a loan can be difficult (banks are in general more risk averse).

Equity investors take more risk by investing money in a company in exchange for shares, meaning they could lose it all. Since an equity investor becomes a shareholder when he/she invests in your company you will (partly) lose control of the firm. Moreover, you will need to share your profits with your new shareholders and sometimes they might want to be actively involved in the management of your company as well.

Of course there are other ways to fund your startup, such as crowdfunding, convertible notes and subsidies.

Conclusion

Why you should always engage in financial modeling as a startup

There are different reasons why to engage in financial modeling as a startup. You might need a financial model to build an economically viable business, to be better prepared for the future, to communicate your company’s performance to potential shareholders or new investors, or to set targets for your company you can work towards.

The two main approaches towards financial modeling are the top down method (leveraging market size data to build a forecast for your company) and the bottom up approach (using internal company specific data such as sales data or data on the internal capacity).

It could be useful to combine both methods as it allows you to substantiate short term targets on a detailed level and it allows you to demonstrate the long term desired market share and the ambition an investor is looking for. No matter what approach is used, a forecast stands or falls based on its underlying assumptions.

Typically, the outputs of a startup’s financial model consist of a three to five (sometimes 10) year forecast of the financial statements on a yearly basis (profit and loss statement, balance sheet, cash flow statement), an operational cash flow overview for the coming 12 months ahead, and an overview of the company or sector specific key performance indicators (KPIs).

These outputs are the results of the calculations taking place in the background of a financial model, based on the data entered into different input pages of the financial model. These input pages consist of, for instance, forecasts of: revenues, cost of goods sold, operating expenses, personnel, investments in assets (capital expenditures) and financing.

For some of the outputs supporting calculations and schemes are required. These include, for example, working capital, depreciation and taxes. Using the data that is typically part of a financial model you are also able of creating a valuation of your startup using the discounted cash flow method.

It can be worthwhile to create several scenarios of a financial model (worst vs. base vs. best case) and to check for common pitfalls in financial modeling for startups. Creating multiple scenarios and performing sanity checks helps you get closer to a realistic case, instead of presenting an overly optimistic or an unattractive case.

Having a financial model can help in the fundraising process, as external financers typically require you to provide a forecast. This makes sense, considering the fact you are asking them to put their money in your company.

There are different sources of funding, the main ones being debt and equity financing. However, more and more sources of funding emerge, such as: convertible notes, crowdfunding, initial coin offerings and, of course, subsidies and grants.

If you have made it all the way to the end of this article: well done! With the information we have shared you are well equipped to start forecasting, maybe even build your own financial model and make sense out of the metrics and data that are presented by your model.

As mentioned earlier there are tons of financial model templates for startups to be found on the web. If you need more support, feel free to reach out to us here!

Source: https://www.ey.com/en_nl/finance-navigator/the-ultimate-guide-to-financial-modeling-for-startups

RỦI RO CỦA BẠN, CHÚNG TÔI SẼ BẢO VỆ

Bạn quan tâm chúng tôi sẽ giúp bạn bằng cách nào?